(PRWEB) April 13, 2009

Considering that the early 1990s, a FICO score has been a common component of home lending decisions in the United States. Throughout the time of rising house values in the new millennium, the score became less important, as the rise in values served to get several borrowers out of difficulty with payment obligations. Now that home values have come crashing down, banks are as soon as once more putting an enhanced value on FICO scores as a figuring out element for lending choices, says Rick Arvielo, president of New American Funding, a fully delegated FHA lender that performs distressed borrowers via effective write-down negotiations and loan modification activities.

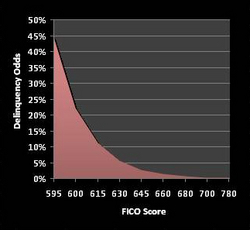

You want only glance at the statistics to see that the odds of a borrower becoming delinquent on his or her mortgage go up a lot more than 100 occasions from a sub-600 FICO score to a 700-plus score. That is massive! Now the banks are hunting at this data with renewed interest, Arvielo says.

Even with the help of the Federal Housing Administration — which essentially doesnt acknowledge FICO — major lenders are just refusing to accept borrowers with sub-600 FICO scores, making FHAs want to give financing to these who may otherwise qualify irrelevant.

I uncover myself puzzled by the telegraphing being accomplished by the industry, which suggests a borrower need to have be in default just before he or she can receive attention from loss mitigation and default prevention possibilities, provided the fact that performing so will destroy your probabilities for a new loan as your all-important FICO will be adversely impaired, Arvielo says. Fannie Maes personal guidance suggests At least two complete monthly payments of principal and interest (P&I), taxes, and insurance (or P&I only if taxes and insurance are not escrowed) are due and unpaid before a homeowner qualifies for support.

With all of this taken into account, the outcome is a landscape where an person will likely need to have to destroy his or her credit worthiness in order to receive the interest price reprieve some most desperately want, regardless of intent. That is really a shame!

FICO credit bureau danger scores are accessible at all 3 main US credit reporting agencies — BEACONsm at Equifax, EMPIRICA