Scottsdale, Arizona (PRWEB) January 12, 2009

Certified Distressed Home Professional (CDPE) Gayle Henderson , of RE/MAX Excalibur in Scottsdale, insists that foreclosure is not the answer to the present residence ownership crisis looming throughout Maricopa County.

December 23, 2008, Henderson was notified by ARMLS (Arizona Regional Several List Program) announcing a pilot plan fostered by Fannie Mae and orchestrated through Countrywide loans to streamline the short sale procedure. “It felt like the greatest Christmas present I could envision,” mentioned Henderson, who is working tirelessly to aid stabilize the housing industry by way of assisting homeowners with loan modifications and short sales. “Arguably, the housing marketplace accompanied by the monetary institutions that lend the cash is the bedrock of our economy,” stated Henderson.

When Bob Bemis, CEO of ARMLS was approached by Fannie Mae as one of five national MLS systems to participate in this pilot system, his reaction was good and supportive. “We need to do one thing about streamlining the brief sale system,” stated Bemis. “And this seems to be a credible plan to test,” he continued.

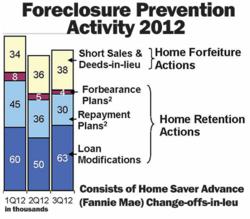

Short sales eligible for this pilot system have been identified as these on the market place as of December eight, 2008. Listing agents of these properties have been contacted by Countrywide to submit the brief sale package on behalf of the seller. Countrywide, in turn, will establish a preapproved sales value which will be reflected throughout the 90-day pilot system as the list price tag. Any price tag adjustments for the duration of the listing period will potentially disqualify the house from the pre-authorized status granted by Countrywide. The plan is designed to expedite the quick sale method, move inventory a lot more swiftly minimizing the lenders loss, while assisting the property owners to stay away from foreclosure.

“Acquiring the word out to Purchasers and Purchasers Agents that short sales are becoming the new attractive house to purchase is essential in helping stabilize our industry,” mentioned Henderson. “The value in acquiring a quick sale is tremendous. The Seller, often, is nonetheless living in the property, maintaining up with routine upkeep each inside and out. The pricing is at existing market place worth. And the condition surpasses most of its foreclosure counterparts.”

“Not understanding the consequences of foreclosure lead a lot of home owners to just give up,” mentioned Henderson. “And believe me there is a distinction in life soon after foreclosure as opposed to life with out foreclosure. We may possibly not be in a position to save each and every residence, but we can provide the saving hand to each financially distressed homeowner. Presently we see lenders are much more receptive to expediting the quick sale approach,” mentioned Henderson. It is important to don’t forget that lenders are not in the organization of acquiring home, they are in the business to lend cash. Assisting to clear these non-performing assets (default loans) from their books will result in a quicker bounce back in this economic crisis.

For a confidential phone interview relating to your true estate concerns, make contact with Gayle Henderson at 602-850-4335.

Gayle Henderson, Pc, CRS, GRI, ABR, CLHMS, E-Pro, CDPE is offered for comment and contribution to Real Estate associated troubles. Get in touch with Gayle Henderson at 602-850-4335 or check out http://www.AZAvoidForeclosureNow.com.

# # #

A lot more Loan Modification Press Releases